About halfway through the month, we thought this report would be focused on the meaningful drawdown to start August and the preceding rally. That theme may still be relevant, but with foreign currency in the news and historically significant performance of our Foreign Currency factor, we decided that a special edition was warranted.

This month we will review the methodology and design of our Foreign Currency factor as well as discuss August and historical results. Before that, let’s take a look at performance for the overall Two Sigma Factor Lens.

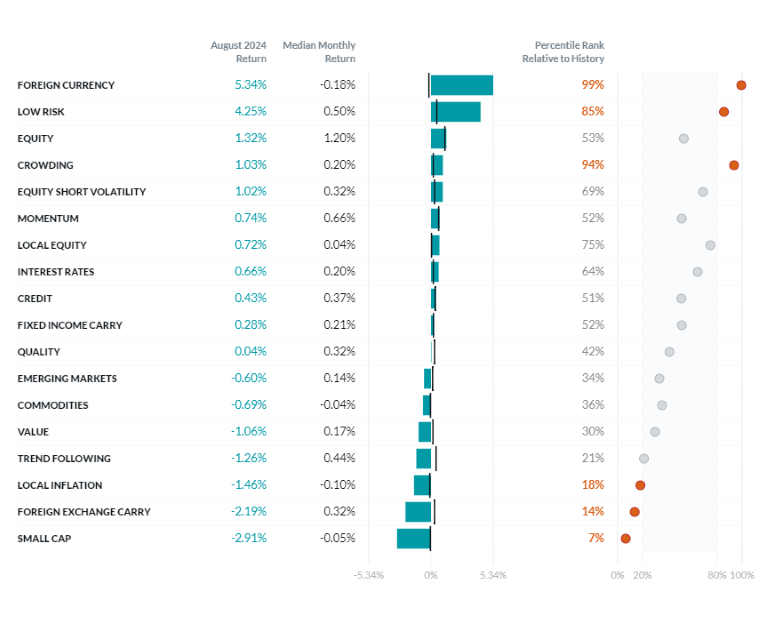

Exhibit 1: August Performance of the Two Sigma Factor Lens

©2024 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures.

Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period Oct 1997 - August 2024

A Refresher on Venn’s Foreign Currency Factor

Venn’s Two Sigma Factor Lens is available in all G10 currencies. Generally, our factors don’t change because they are designed to neutralize currencies. For example, our Equity factor is currency hedged, so its perspective does not depend on an investor's local currency.

Unlike Equity, the meaning of Foreign Currency factor exposure is completely dependent on which currencies are considered foreign, and thus changes based on the currency lens being used. Specifically, Venn’s Foreign Currency factor measures a GDP-weighted basket of G10 currencies relative to an investor's local currency, accounting for both spot price movements and cash rate differentials. Practically speaking, Venn has 10 different Foreign Currency factors.

Additionally, we have found that other factors can be correlated with movements in global exchange rates. As a result, we aim to make our Foreign Currency factor uncorrelated with our core macro factors: Equity, Interest Rates, Credit, and Commodities. This ensures that when users measure their beta, risk, or return driven by our Foreign Currency factor, the results aim to represent a purer exposure to exchange rates and cash rate differentials. You can read more about how factor independence is inherent in Venn’s philosophy here.

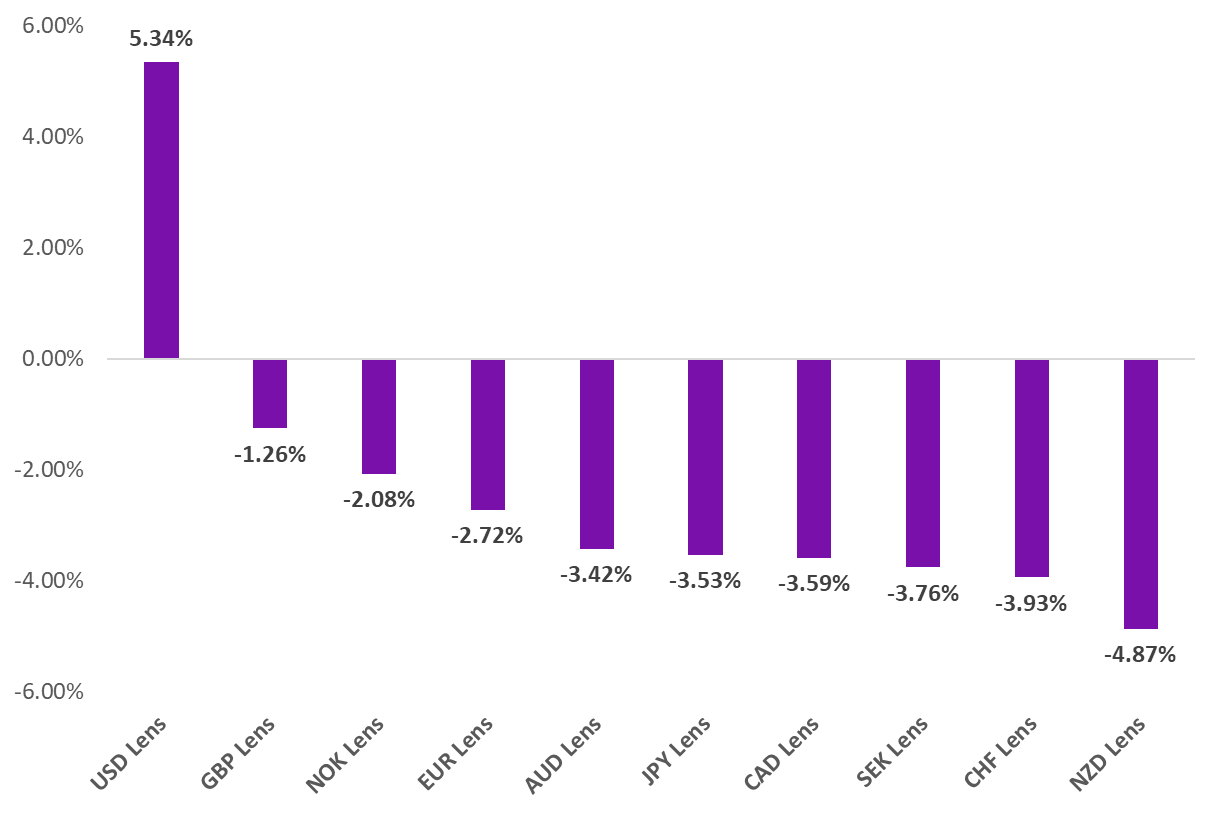

August Performance for Venn’s Foreign Currency Factors

While foreign currencies are often discussed in relative terms, Venn’s Foreign Currency factor aims to explain the broad risk and return across many foreign currencies versus a single local currency.

In August, investors based in G10 currencies faced Foreign Currency factor headwinds, with the notable exception of US-based investors who benefited significantly.

Exhibit 2: August Performance of Venn’s Foreign Currency Factors

Source: Venn by Two Sigma

A variety of themes help to explain August USD weakness, which led to US investors benefiting from Foreign Currency factor exposure. Dovish Fed talk to end July and throughout August has promoted a weakening dollar, while the BOJ has been hawkish, including conducting a rate hike.1 As we wrote in last month’s report, shrinking interest rate differentials led to an unwind in the popular USD/JPY carry trade, causing investors to close their short JPY positions and exit their long USD. This carry unwind accompanied by impending rate cuts compounded into meaningful USD weakness.

Other market participants have argued that the broadness of the weakening USD, not just against the JPY, may be due to shifting expectations for the upcoming presidential election. As Harris gains ground and a Democratic victory becomes more possible, the USD may be weakening in response (the idea being that Trump and his policies are more associated with a stronger dollar).2

No matter the cause, the USD was down -2.31% in August,3 sending shockwaves throughout foreign currency markets.

Historical Foreign Currency Factor Returns

At this point, we have established that, broadly speaking, investors outside of the US were punished in August for taking on Foreign Currency factor risk, but what about historically?

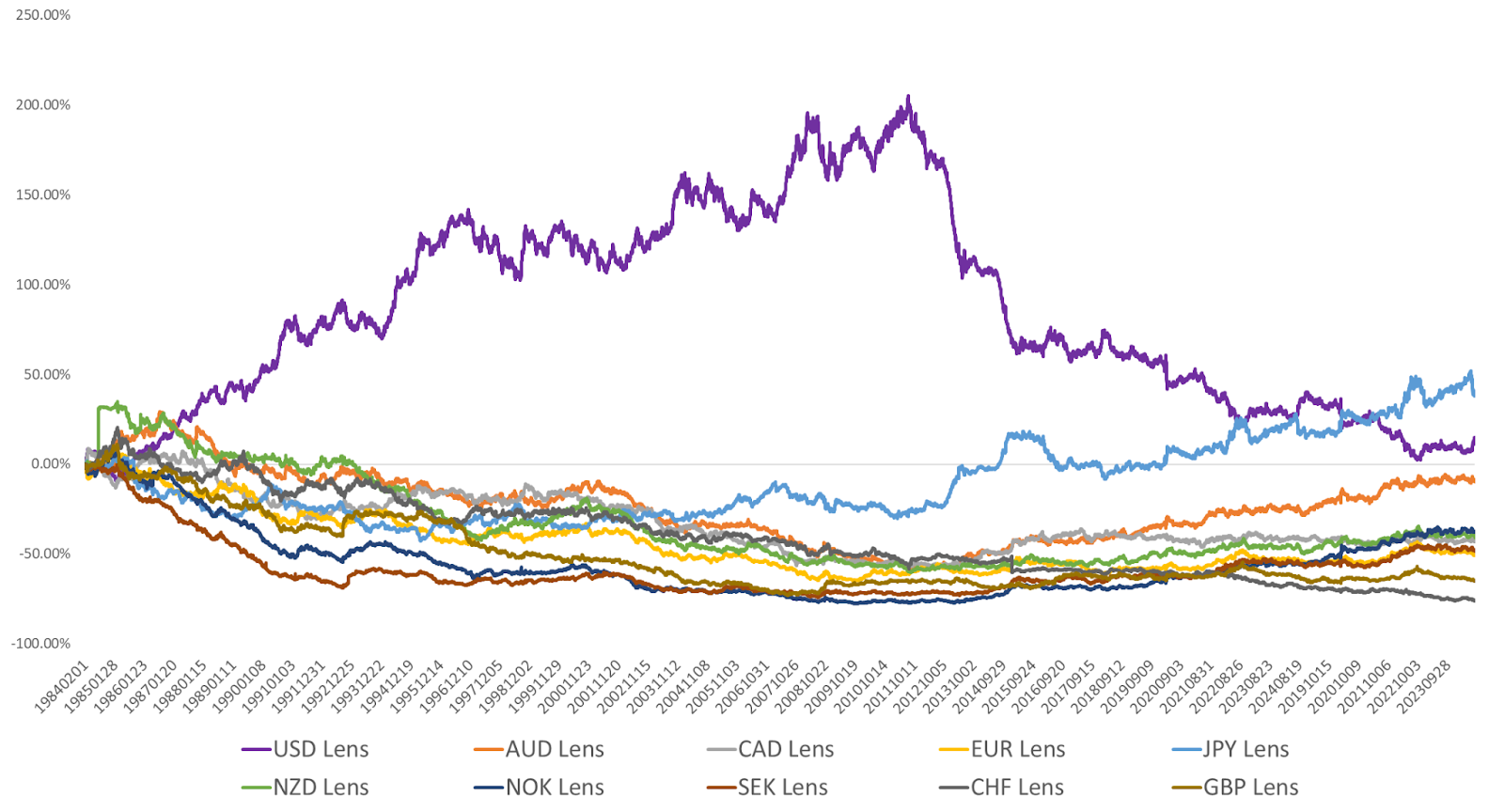

Below, we show all ten of Venn’s Foreign Currency factors back to their common period starting in 1984.4 Remember, these factors represent broad foreign currency returns versus an investor’s local currency, after being separated from our Equity, Interest Rates, Credit, and Commodities factors.

Exhibit 3: Historical Cumulative Returns of Venn’s Foreign Currency Factors

Source: Venn by Two Sigma

According to Exhibit 3, only US and Japanese investors have been rewarded for Foreign Currency factor exposure historically, with JPY investors benefiting the most. A clear standout in Exhibit 3 is the directional change for US-based investors around 2011, which is when Foreign Currency factor exposure started to become a meaningful headwind. This coincided with several events, including completion of US quantitative easing and the continued recovery of the US economy post the global financial crisis.

The Role of Foreign Currency

A critical point to understand is that there is not a strong case for Foreign Currency factor exposure to be a driver of alpha over time. In fact, many of Venn’s factors are not associated with alpha, but rather, aim to explain the return and risk of multi-asset portfolios.

Currently the USD and JPY are making headlines, but the USD even more so as the US continues to flirt with rate cuts and finally seems ready to make the first move. Investors with exposure to foreign currencies, or unhedged international assets, would be wise to consider a Foreign Currency factor when diversifying their portfolio and understanding their drivers of risk, especially in the current environment.

References

1 https://www.reuters.com/markets/feds-dovish-shift-mixed-blessing-boj-rate-hike-plan-2024-08-23/

3 As measured by the DXY Index

4 Shout out to the Plaza Accord, starting off the USD’s significant depreciation in the mid-80s.

References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.